The wealth tax Impuesto sobre el Patrimonio IP (Model 714) in Spain was initially introduced as a temporary measure, but for many years it continues to be “successfully” levied on individuals: both from residents of the country and from non-resident foreigners.

Who is required to file a Model 714?

NON-RESIDENTS:

- If, as of December 31 of the reporting year, the aggregate valuation of movable and immovable property without encumbrances exceeded 700,000 euros. This includes the assessment of funds in current accounts or deposits, the assessed value of real estate in Spain, cars (if there is no double taxation agreement between the non-resident country and the Kingdom of Spain).

- If on December 31 of the reporting year the aggregate appraisal of movable and immovable property exceeded 2,000,000 euros, even if the amount of encumbrances (for example, a mortgage on a house) exceeds the amount of assets.

Tax residents of other EU countries have a special position , they can decide whether to pay tax at the state rate or at the regional rate (where the main part of their wealth is located in Spain).

Non-residents, on the other hand , are always subject to a single state rate and do not have any tax breaks, unless otherwise provided by the Agreement on Double Non-Taxation between the non-resident country and the Kingdom of Spain. So, for example, residents of the Russian Federation in the tax return are officially exempted from including cars in the tax base.

RESIDENTS

- If as of December 31 of the reporting year, the aggregate valuation of movable and immovable property without encumbrances exceeded the lower threshold for taxation. It is different in each region, for example, Catolonia, Extremadura – 500 thousand euros, Aragon – 400 thousand euros, Navarra – 550 thousand euros, Valencia – 600 thousand euros, the Basque Country – 800 thousand euros. In Andalusia, Cantabria, Asturis, Castilla and Leon, Castilla La Mancha, Galicia, Murcia, the Balearic and Canary Islands – 700,000 euros. In Madrid, the wealth tax is not paid!

The IP rate varies on average from 0.2 to 2.5% and may differ in different autonomies (for example, Extremadura set the maximum rate at 3.75% and Catalonia – at 2.75%). The level of the applied rate depends on the value of the property, that is, the more expensive it is, the higher the rate for calculating the amount payable.

Nevertheless, in some of these regions, bonification is assumed for real estate, permanent residence of the resident.

Taxed: real estate objects, bank accounts, jewelry, vehicles, art objects, valuable antiques, income from intellectual property rights – their aggregate value as of December 31 of the reporting year.

“New residents” who only became tax residents in Spain in 2019 were required to submit Model 720 by the end of March (about property worldwide over 50 thousand euros) More details can be found here: https://prospainconsulting.com/2017/05 / 18 /% d0% bd% d0% b0% d0% bb% d0% be% d0% b3% d0% b8-% d0% b4% d0% bb% d1% 8f-% d1% 80% d0% b5% d0% b7% d0% b8% d0% b4% d0% b5% d0% bd% d1% 82% d0% be% d0% b2-% d0% b8% d1% 81% d0% bf% d0% b0% d0 % bd% d0% b8% d0% b8-% d0% bc% d0% be% d0% b4% d0% b5% d0% bb /

Accordingly, on its basis, Model 714 will already be submitted, where property in Spain must be added to all property.

Calculation example:

NON-RESIDENT

PHASE 1: tax base: 720,000 + 375,000 + 114,500 = € 1.209.500

Burden: no

PHASE 2: TAX MINIMUM DEDUCTION – € 700,000

LIQUID BASE: € 509,500

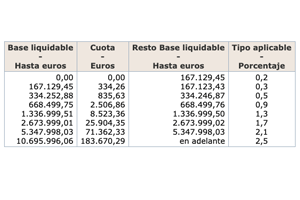

PHASE 3: payable 1711, 86 euros. Consists of:

- EUR 835.63 related to EUR 334.252.88 BASE LIQUIDABLE by table

- € 876.23 relating to the remaining € 175.247, € 12 (509.500-334.252.88) multiplied by 0.5%

Calculation example:

RESIDENT (CATALONIA)

PHASE 1: tax base: 720,000 + 375,000 + 114,500 = € 1.209.500

Burden: no

PHASE 2: TAX MINIMUM DEDUCTION – € 700,000

LIQUIDABLE BASE: 500,000

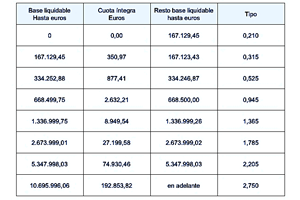

PHASE 3: payable 3019, 66 euros. Consists of:

- € 2,632.21 related to 668,499.75 LIQUIDABLE BASE in Table 2

- € 387.45 related to the balance € 41,000.25 (709,500 – 668,499.75) multiplied by 0.945%

Comments (0)